Enduring the Wrong Trade for the Right Reasons

Parsing drawdown through macro analysis

Disclaimer:

All content in this publication reflects my personal opinions and is for informational purposes only. It does not constitute financial, investment, legal, or tax advice. Always conduct your own research and consult a licensed professional before making any decisions.

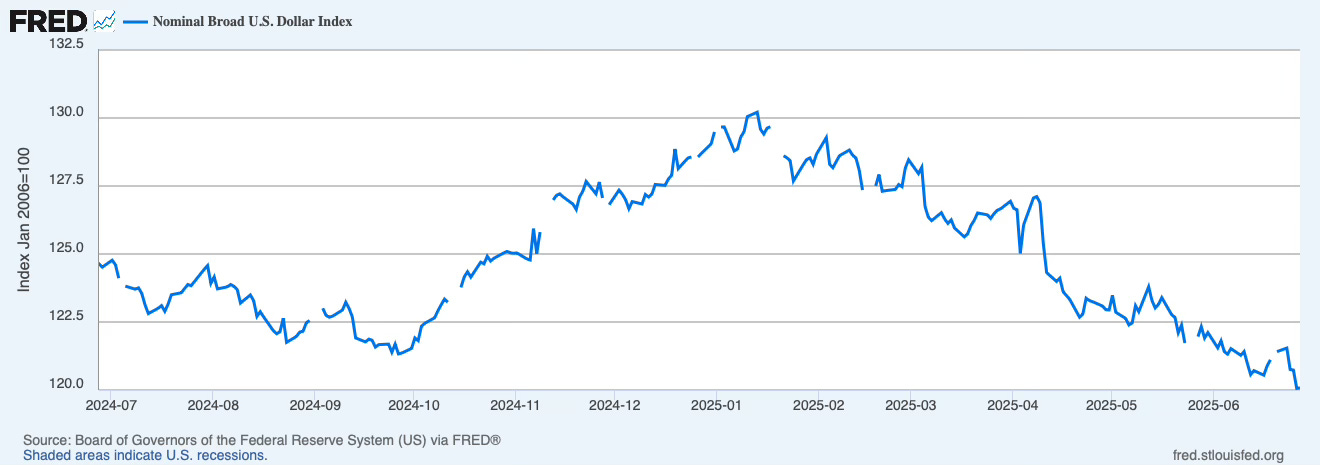

For those who’ve followed my work, you’ll know I’ve been building into substantial Dollar-long positions [spot and leveraged] for weeks now. These are large allocations, structured around a conviction that inflation pressures would resurface and reprice global FX markets accordingly.

And yet, the Dollar continues to make lower lows.

Drawdowns have grown. That’s the nature of directional macro: you’re either early or wrong until proven otherwise.

I take advantage of periods like this to force a return to first principles. Not emotional recalibration, but a methodical reexamination of the original thesis—checking whether what’s changed is the macro landscape, or just market perception.

What follows are the exercises I conduct to stay intellectually honest when price moves against my initial thesis — the macro framework I use to remain as objective and impartial as possible.

Dollar Weakness That Doesn’t Follow the Script

In textbook macro-economics, tariffs tend to be dollar-positive.

They raise import prices, push inflation higher, and—under a rules-based monetary regime—invite tighter financial conditions through higher real yields. Those higher yields, in turn, should attract capital inflows, lending strength to the Dollar.

But this time, the Dollar fell.

Not sharply, but persistently—and in direct defiance of the models that typically guide FX reaction functions. So the question becomes: what’s different?

The answer lies not in the inflation impulse or yield mechanics, but in the market’s conviction—or lack thereof—regarding the durability of U.S. policy.

Traders aren't buying the idea that tariffs under a second Trump administration are “real” in the way macro theory assumes. They're not seen as structural, enforceable, or even consistent. They are, in effect, being priced as performative rather than strategic—rhetorical devices in a political toolkit rather than long-term tools of economic engineering.

This growing detachment between policy announcement and policy belief is more than a quirk of political theater. It reflects a shift in how markets are modeling U.S. credibility. Investors are no longer pricing outcomes based on the mechanics of tariffs, but on the trustworthiness of the regime implementing them.

Take the ambiguity around the Trump campaign’s posture toward Russia.

It signals that American foreign policy—once treated as path-dependent and alliance-bound—is now perceived as transactional and reversible. The implication is simple but far-reaching: if the U.S. can pivot quickly on Russia, it can just as easily reverse course on China, rendering today’s tariffs tomorrow’s tweet-fodder.

This erodes not just the perceived permanence of policy but the very foundation upon which the Dollar’s reserve status rests: strategic consistency.

To be clear, this isn’t about inflation or deficits or trade balances—not directly. It’s about credibility drift. When global markets can no longer assume continuity in American policy, they begin to treat the Dollar not as a stable benchmark, but as a variable. And in a system built atop that benchmark, uncertainty multiplies outward.

What we’re witnessing isn’t just a weak Dollar; it’s a Dollar whose weakness reflects doubts about the United States' capacity to act as a predictable steward of the global financial order.

And when that faith wavers—even at the margin—emerging markets, commodity exporters, and minor allies begin to hedge not just their exposures, but their alignments.

Market Perception vs. My Thesis

At the moment, market consensus is leaning dovish.

Recent inflation data—muted, in some cases even below expectations—has led traders to position for a more accommodative Fed relative to its G10 peers. In the FX space, this has translated into persistent Dollar softness, as the U.S. yield advantage compresses.

But that interpretation misses the plot.

What markets are treating as evidence of structural disinflation is, in my view, a mirage. The recent softness in CPI isn’t reflective of genuine demand-side weakness or a durable deflationary trend—it’s a lagging artifact of three key distortions:

The delayed pass-through of newly imposed tariffs.

Post-pandemic seasonal anomalies baked into official data.

Temporary tariff circumvention tactics that mute cost pressures (for now).

These aren’t sustainable dynamics.

They’re statistical and logistical shadows that will fade with time, and when they do, the underlying inflation pressure—cost-push in nature—will reassert. As it does, the Fed will be forced to recalibrate. A monetary stance that markets currently view as soft will turn more hawkish, not because the Fed wants to, but because the economic data will eventually strip away its plausible deniability.

And when that pivot occurs, it won’t just impact rates. It will likely ripple across asset classes, including FX.

U.S. yields will rise, rate differentials will widen, and the Dollar—currently caught in a pessimistic overshoot—will begin to reverse course.

A Turning Point in the Dollar Cycle

If we zoom out, the current Dollar weakness doesn’t mark a structural decline—it marks the bottom of a cyclical trough, distorted by temporary forces. The inflation lull is just that: a lull, not a landing.

Front-loaded inventory buildups ahead of tariff enforcement have delayed inflation visibility. Transshipment workarounds have blunted the early impact of those tariffs. And seasonal models still warped by COVID-era data have introduced further noise into inflation readings.

But those buffers are eroding.

By late Q3 or Q4 of 2025, the deferred inflation shock is likely to arrive—once inventory cushions deplete and tariff circumvention routes are closed or sanctioned.

As price pressures return, the Fed will either have to hold the line or tighten further, even as Europe and other G10 economies move in the opposite direction, grappling with disinflation tied to global demand softness.

This divergence in policy paths will reset the relative rate narrative—and with it, the trajectory of the Dollar.

Also at play is sentiment.

FX positioning has grown reflexively bearish toward the Dollar, extrapolating today’s softness into tomorrow’s policy. But markets are rarely that linear. When the inflation data turns—and it will—positioning could snap violently back in the other direction.

Not Structural Weakness—Strategic Mispricing

The Dollar’s decline is not a structural verdict on U.S. economic fundamentals. It is, rather, a reflection of geopolitical ambiguity, temporary data distortion, and overextended narrative cycles. Markets have mistaken noise for signal, and short-term disinflation for long-term accommodation.

The more durable threat to the Dollar isn’t inflation, tariffs, or even deficits—it’s credibility. It’s the perception of whether U.S. policy is coherent, rules-based, and strategically anchored. If the world believes America can still act as a consistent steward of global systems, the Dollar will recover. If not, the erosion won’t show up in CPI prints or GDP—it’ll show up in hedging behavior, trade invoicing, and reserve diversification.

In that sense, the coming move in the Dollar won’t just be about rates. It will be about belief.

Tariffs: Misunderstood, Not Ineffective

In theory, tariffs are inherently inflationary.